Summarize this blog post with:

Editor’s Note: Productivity gains have become the "baseline" of the AI era “which are important”, but no longer a competitive differentiator. The real ROI is migrating toward the middle tier of the hierarchy: Decision Intelligence. Through this blog see why the middle of the AI pyramid is currently underinvested and how the rise of agentic architectures is finally allowing enterprises to bridge the gap between fragmented data and high-stakes execution.

Worldwide AI spending will hit $2.52 trillion in 2026 — up 44% YoY per Gartner — with 86% of companies increasing AI budgets. AI has graduated from experiment to operating line item.

Yet ask executives what their systems are doing and the answers cluster narrowly: summarising documents, drafting emails, writing code faster, deflecting support tickets. Important work. But for a technology that promises to reshape industries, the ambition feels underwhelming. Hence treating AI as a pure productivity multiplier is correct, but incomplete. It is like describing electricity as a better candle which would have missed refrigeration, radio, and the assembly line entirely.

And hence what we are seeing is a similar pattern unfolding with AI.

When we study where enterprises are deploying AI, and more importantly, where they are capturing measurable value, a pattern emerges. The returns cluster across three-time horizons, varying defensibility, and distinct competitive consequences.

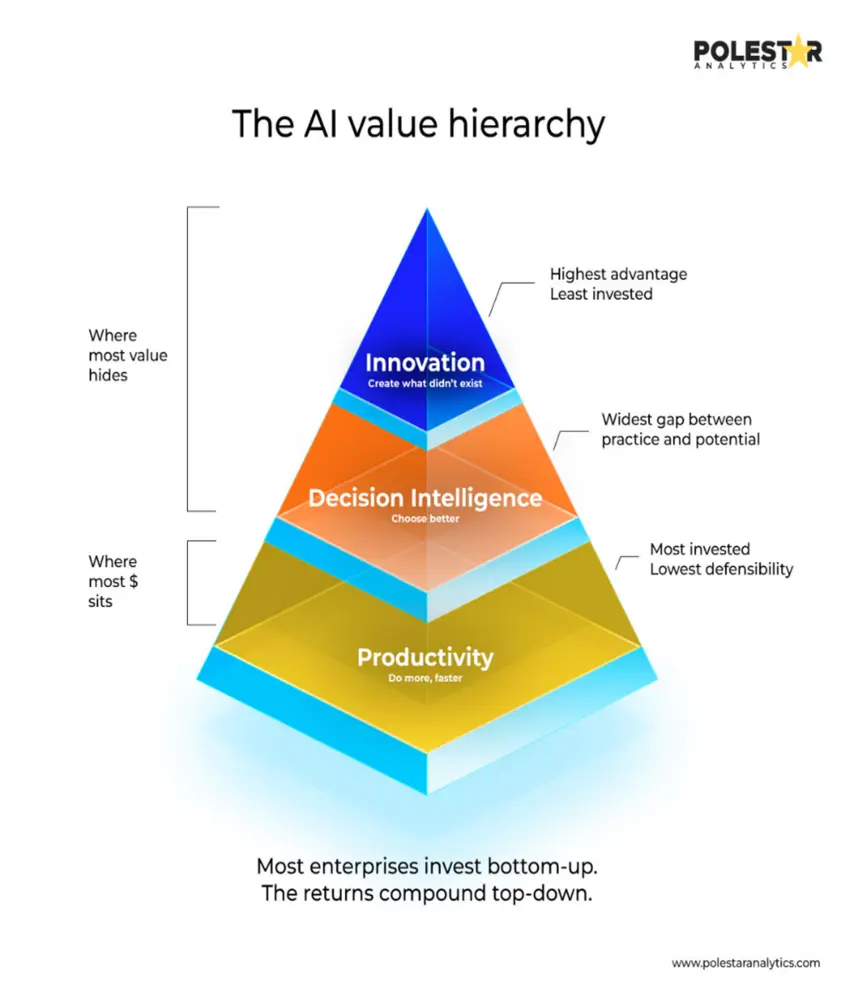

The AI Value Hierarchy

The AI Value Hierarchy

Tier 1 — Productivity

Where most spend lives. Copilots, assistants, and automation tools help teams produce more output per hour. Deloitte's 2026 State of AI report finds two-thirds of enterprises report efficiency gains — more than any other benefit. But productivity has a structural ceiling: the same tools are available to every competitor, so the advantage commoditises. This creates a structural imbalance.

Tier 2 — Decision Intelligence

Far less crowded, far more powerful. AI does not execute existing decisions faster — it improves the decisions themselves. A productivity tool helps an analyst write a report in two hours instead of eight. An AI decision intelligence platform tells that analyst the conclusion is wrong because an underlying assumption changed three weeks ago. This applies across pricing, capital allocation, supply chain, and risk. This is where AI changes what gets decided, not just how fast it gets done.

Tier 3 — Innovation

Capabilities that didn't previously exist — three-person teams launching what required thirty; AI-discovered drug candidates in late-stage trials. Innovation cannot be replicated off-the-shelf; it emerges from proprietary data, domain expertise, and new questions worth asking. Making it the highest tier which is most transformative.

Productivity improvement gets you there that requires a fundamentally new capability.

Build smarter decisions with our AI experts.

Connect your data, decisions, and execution with agent-native AI built for real business impact.

Get in touch with our AI experts

Most enterprises are investing from the bottom of this hierarchy upward.

The overwhelming majority of spend sits at the productivity tier. Deloitte's survey found that only 34% of organisations are using AI to deeply transform their business. Another third are redesigning key processes. The remaining third are applying AI at the surface level, with little or no operational change. Everyone is getting productivity gains. Very few are building decision advantage. Fewer still are pursuing genuine innovation.

The pattern is understandable. Productivity tools are the easiest to deploy, the simplest to measure, and the most immediately gratifying. But the strategic risk is real: if AI strategy is exclusively productivity-focused, the investment concentrates in the tier with the lowest defensibility and the fastest path to commodity status — buying faster legs in a race where the winners are building airplanes.

Enterprise AI budgets grew 75% year-over-year, according to a survey of 100 CIOs by Andreessen Horowitz. Innovation budgets dropped from 25% of AI spend to just 7%. AI has moved from experiment to operating expense. The question is whether the operating expense is pointed at the right tier of value.

If decision intelligence is the tier with the most asymmetric returns, why is it the most underinvested? Because it is hard in a way that productivity AI is not.

Deploying a copilot for email is a configuration exercise. Deploying a system that improves decisions is fundamentally different. It requires connecting fragmented data across systems that were never designed to talk to each other. It requires domain expertise to distinguish signal from noise. It requires trust, built over time, in outputs that challenge institutional assumptions. And it requires operating at the cadence of the decisions being made, not the cadence of a quarterly review.

None of this was possible at enterprise scale until very recently. Three shifts have changed the equation:

- Data infrastructure has reached critical mass. Two decades of ERP, warehouses, and analytics built the substrate. The missing piece — synthesis at speed — is finally available.

- Agentic architectures have emerged. Decision intelligence systems no longer wait for the right question. They monitor signals, form hypotheses, and initiate action.

- Traditional cost levers have exhausted themselves. Hiring freezes and broad cuts now produce diminishing returns. Companies need precision, not austerity.

The infrastructure is finally ready. Most organisations simply have not connected it to the decisions that matter most.

Decision intelligence applies across many domains — pricing, capital allocation, talent deployment, operations, risk. The asymmetry is most visible in one place: external spend.

The cost of goods, materials, and services purchased from external parties routinely represents 50 to 70% of total revenue in manufacturing, more than 60% in retail, and 30 to 40% even in professional services. In most companies it is the single largest line in the P&L. Payroll, for all the attention it receives, typically represents only 15 to 30% of revenue for product-oriented firms.

When companies deploy AI for cost management, the first instinct is almost always to target labour — automate call centres, reduce processing headcount, compress cycle times. These are valid applications, but they target the smaller variable. A dollar saved on external spend is a dollar of EBITDA. No reorganisation, no change-management programs, no translation loss between "capacity created" and "cost removed."

The patterns repeat across industries. A global manufacturer found its commodity pricing was above market benchmarks, not because of poor negotiation, but because the team lacked real-time visibility across geographies. A financial services firm discovered software licences that were inactive or underutilised, creating avoidable waste because no team could connect procurement records, usage data, and contract terms at the right cadence. An industrial company was also failing to enforce its own contract terms, leaving rebates, escalation clauses, and volume discounts unclaimed.

None of these are productivity problems. None of them are solved by making people work faster. They are solved by making the organisation see what it currently cannot see, and act on what it currently cannot process.

These problems are not new. What is new is that the technology to address them finally exists.

Build smarter decisions with our AI experts.

Connect your data, decisions, and execution with agent-native AI built for real business impact.

Get in touch with our AI experts

External spend is illustrative, but the dynamic is not unique to it. The same pattern repeats anywhere high-value decisions are made under conditions of information scarcity and cognitive overload.

Capital allocation runs on backward-looking models that cannot incorporate real-time market signals. Pricing relies on spreadsheet-based competitive analyses that are obsolete the week they are built. Risk assessments depend on point-in-time snapshots that miss emerging threats. Resource deployment is guided by heuristics that have not been tested against data.

The pattern is the same: the decision is important, the information needed to make it well exists somewhere, but no human team can synthesise it at the required speed and scale. So decisions get made with whatever is readily available — which is almost never enough.

This is the gap decision intelligence fills. Not by replacing human judgment, but by arming it with information that was previously too expensive, too slow, or too complex to obtain. And it creates a form of competitive advantage that productivity AI cannot. Productivity tools are horizontal — the same copilot works the same way for every company. Decision intelligence is inherently proprietary: built around your data, your patterns, your operating context. It learns from a specific environment and compounds in value over time. It cannot be replicated by a competitor deploying the same off-the-shelf software.

This is not an argument against productivity AI. Companies need it. But the portfolio across most enterprises is dramatically out of balance.

Investment is concentrated in the tier with the lowest ceiling and the least defensibility. The tier with the widest gap between current practice and what is now possible — decision intelligence — remains underfunded. And the tier where AI enables genuinely new capabilities has barely been explored.

For the CFO, the implication is direct. Productivity AI returns are real but bounded; they will flatten as tools commoditise and every competitor reaches parity. Decision intelligence returns are asymmetric and compounding. They create proprietary advantage — and often fund the innovation investments that produce the most transformative outcomes.

The companies that will lead in the next decade are not the ones that deploy AI most widely. They are the ones that deploy it most wisely.

The AI conversation in most boardrooms is dominated by a single question: How do we make our people more productive?

It is the right question, asked too narrowly.

The fuller question is: What can our organisation now see, decide, and do that it simply could not before?

Three answers emerge.

- We can do what we have always done, faster — that is productivity, necessary but not sufficient.

- We can make better choices about how resources, capital, and attention flow through the organisation — that is decision intelligence, where most companies have the widest gap between current performance and what is now achievable.

- We can create entirely new products, services, and capabilities that did not previously exist — that is innovation, the ultimate competitive advantage, often built on the foundation laid by the first two tiers.

Most enterprises have invested heavily in the first answer. Very few have seriously pursued the second. Almost none have structured their AI programs around the third.

That imbalance is both the strategy problem and the opportunity. Decision intelligence is where the next decade of advantage will be won — and where forward-leaning enterprises should be directing their AI investment now.